World4Solar – KNOWLEDGE BASE

How Smart U.S. Companies Save Massive On Taxes With Solar In 2024

Contents in this article

1. Introduction To Federal Incentives For Solar Energy Systems

2. Investment Tax Credit (ITC)

3. Production Tax Credit (PTC)

4. MACRS Depreciation Benefit (Commercial Only)

5. Direct Pay / Elective Pay (Tax-Exempt Entities Only)

6. Domestic Content Bonus

7. Energy Community Bonus

8. Low-Income Community Bonus

9. Detailed Example Calculations

10. Conclusion

FAQ

Introduction To Federal Incentives For Solar Energy Systems

In an era where economic efficiency meets environmental responsibility, the United States federal incentives for solar energy investments in 2024 present a compelling case for businesses and individuals alike. The Investment Tax Credit (ITC) and Production Tax Credit (PTC), alongside accelerated depreciation options under MACRS, are pivotal in reducing upfront costs and enhancing returns on investment in solar technology. With provisions like the Domestic Content Bonus and Direct Pay, these incentives not only lower tax liabilities but also bolster the domestic manufacturing sector, align with sustainable practices, and support community development. This article explores these incentives in depth, offering actionable insights into how they can significantly decrease the financial burden of adopting solar solutions, thereby making a substantial impact on the renewable energy landscape.

Investment Tax Credit (ITC)

The Investment Tax Credit (ITC), also known as the federal solar tax credit, is a significant financial incentive for businesses and individuals investing in solar energy systems in the United States. Here are the key features of the ITC:

- Credit Amount: The ITC allows you to deduct 30% of the cost of installing a solar energy system from your federal taxes. This rate applies to systems installed between 2022 and 2032. After 2032, the credit rate decreases—26% in 2033 and 22% in 2034.

- Eligible Projects: The credit can be applied to both residential and commercial installations. It covers the solar PV system costs including the equipment and installation expenses. For businesses, it also includes solar battery systems if the battery is charged by the associated solar system.

- No Maximum Limit: There is no cap on the value of the credit; it is based purely on a percentage of the investment costs.

- Roll-Over Benefit: If the federal tax credit exceeds the tax liability, the excess amount can be carried forward to the next tax year, enhancing flexibility for investors to fully benefit from the credit.

If a business or individual spends $100,000 on a solar installation, they can claim a $30,000 tax credit to offset their income taxes due that year. To claim the credit, taxpayers must complete IRS Form 5695 (for homeowners) or IRS Form 3468 (for businesses) as part of their tax return. They need to calculate the credit on this form and then add the result to their general tax form (1040 or 1040-SR).

The ITC remains a cornerstone policy mechanism in the U.S. for promoting renewable energy installations and is a critical factor in financial planning for businesses and individuals considering solar energy investments.

Further info about the ITC here >>

Year

Deductable Amount through ITC

2022 – 2032

30%

2033

26%

2034

22%

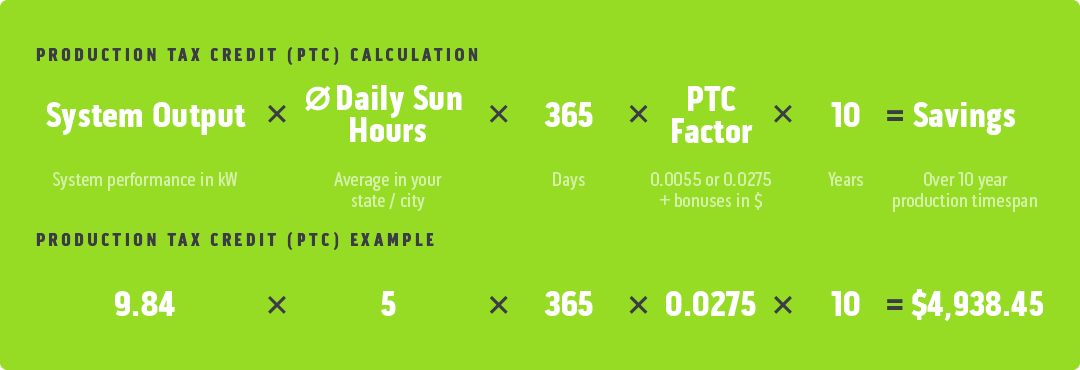

Production Tax Credit (PTC)

The Production Tax Credit (PTC) for solar energy in the USA has been revived and revised under the Inflation Reduction Act of 2022. This credit now offers a per kilowatt-hour (kWh) incentive for electricity generated by qualifying solar energy systems for the first 10 years of operation. As of now, the rate for solar energy under the PTC is initially set at 0.55 cents per kWh but can increase to 2.75 cents per kWh if the project meets specific labor standards, including paying prevailing wages and meeting apprenticeship requirements or is below the size of 1 Megawatt. It is advised to ask your potential installer if they comply with these requirements for larger projects before signing a contract if you decide for the PTC.

Additionally, the PTC includes bonuses for meeting domestic content requirements and for projects located in designated energy communities, or areas of low income, which can each add an extra 0.3 cents per kWh to the base rate. To qualify for these enhanced credits, specific conditions related to the sourcing of materials and the economic characteristics of the project location must be met.

For solar projects, this shift to offering a PTC provides a significant incentive to enhance production capacity and sustainability, aligning with broader federal goals for clean energy and job creation in the renewable sector.

It is important to mention, however, that the PTC is not stackable with the ITC, which means you have to decide for one or the other. Generally, they both hold a good potential for decreasing the costs for a commercial solar project, with the ITC offering a direct and upfront rebate through a federal income tax credit, whereas the PTC pays off over time (first 10 years of operation) and depending on the actual performance of your system. A general rule of thumb would be: The better the spatial conditions of your system (location, system orientation, sun hours, shade) and / or the bigger your system, the more likely it is that the PTC is your better choice. Therefore, the ITC is more favorable for smaller (residential) sized systems or systems that are located in less sunny areas. However, by choosing the PTC over the ITC, you are eligible for a higher MACRS Depreciation.

Further info about the PTC here >>

Rate Model & Bonuses

Base Rate Amount

Full Rate Amount

Base Credit

0.55 cents

2.75 cents

Domestic Content Bonus

+ 0.1 cents

+ 0.3 cents

Energy Community Bonus

+ 0.1 cents

+ 0.3 cents

Low-Income Community Bonus

+ 0.1 cents

+ 0.3 cents

MACRS Depreciation Benefit (Commercial Only)

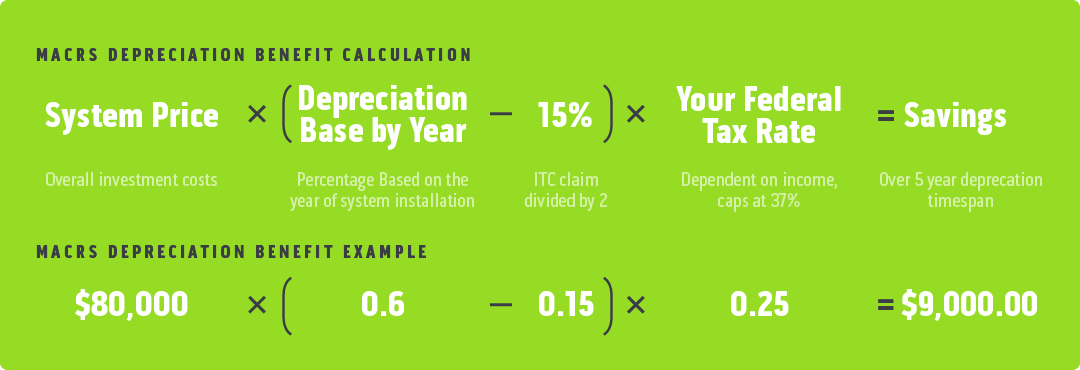

The Modified Accelerated Cost Recovery System (MACRS) is a depreciation method that enables businesses to recover investments in certain property types, including solar PV systems, through accelerated depreciation deductions. For solar installations, MACRS allows the value of the system to be depreciated over a five-year period, which can significantly reduce tax liability and enhance the return on investment.

Under the current regulations, businesses can apply a “bonus depreciation” rate to the initial cost of their solar equipment. For assets placed in service in 2024, this rate is 60%. This bonus depreciation is part of a phase-down schedule established by the Tax Cuts and Jobs Act of 2017, with the rate scheduled to decrease annually until it phases out in 2027.

When utilizing the MACRS benefit in conjunction with the federal Investment Tax Credit (ITC), the depreciable base of the solar system must be reduced by half of the ITC value. For instance, if a business in 2024 claims the 30% ITC, then only 45% of the system’s cost is eligible for depreciation under MACRS (60%-30%/2).

These incentives are structured to encourage more rapid investment in solar technologies by allowing businesses to decrease their taxable income through higher upfront deductions on their tax returns. It’s worth noting that, while MACRS offers significant financial benefits, the specifics of applying these rules can be complex, and it’s often recommended to consult with a tax professional to ensure compliance and optimal tax treatment.

Further info (calculation guide) >>

Further general information from SEIA >>

Year

System Cost Depreciation Base

System Cost Depreciation Base with Full ITC subtraction Applied

2017 – 2022

100%

85%

2023

80%

65%

2024

60%

45%

2025

40%

25%

2026

20%

5%

2027

0%

0%

Direct Pay / Elective Pay (Tax-Exempt Entities Only)

“Direct pay” or “elective pay” significantly influences investment in solar energy systems by allowing eligible entities, particularly those with limited or no tax liability (like tax-exempt organizations, state and local governments, and tribal governments), to receive the value of certain tax credits as direct payments. This means they don’t have to wait to recoup the value of these credits through future tax returns. Instead, they can get immediate financial benefit, making solar projects more financially feasible and attractive.

This mechanism effectively broadens the range of entities that can directly benefit from renewable energy incentives, such as the Investment Tax Credit (ITC) or Production Tax Credit (PTC), by bypassing the need for these entities to have taxable income against which to claim a credit. By enabling a direct cash payment, it reduces the complexity and uncertainty of financing solar projects for these organizations, which might otherwise struggle to leverage tax equity markets.

Application through pre-filing document >>

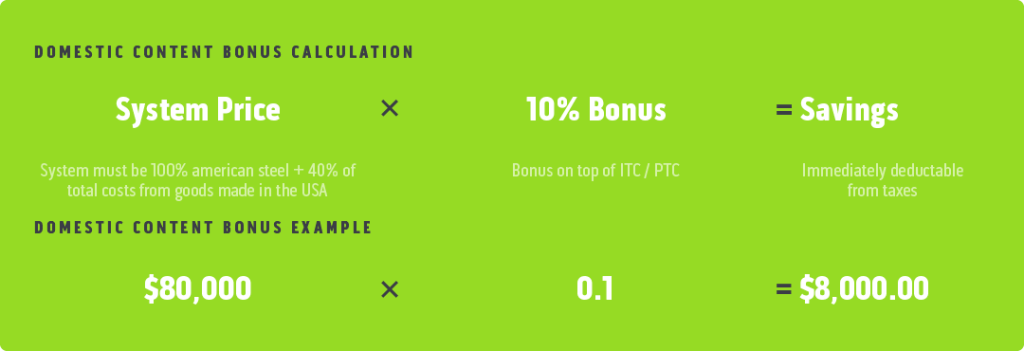

Domestic Content Bonus

The Domestic Content Bonus is an important provision in the Inflation Reduction Act that aims to boost American manufacturing and ensure that the growth of the clean energy economy benefits U.S. workers and companies. This incentive is part of a broader strategy to strengthen the U.S. supply chain for renewable energy technologies and create high-quality jobs domestically.

The Domestic Content Bonus is stackable with the Federal ITC or PTC. In case of an qualifying system, that means:

- Production Tax Credit (PTC): Systems / Facilities that meet domestic content requirements can receive a 10% bonus on top of the standard PTC rate. This means that eligible projects can earn additional credits per kilowatt-hour (kWh) of electricity produced.

- Investment Tax Credit (ITC): Projects that satisfy the domestic content requirements can receive an extra 10-percentage-point increase on the ITC. For example, instead of the standard 30% ITC, a project might be eligible for a 40% credit.

The basic requirements for any system to qualify for the domestic content bonus are the following:

- Steel and Iron: 100% of any steel or iron components of the facility must be produced in the United States. This requirement applies to materials such as rebar and structural steel used in construction.

- Manufactured Products: At least 40% of the total costs of the manufactured products used in the facility must be attributable to products that are mined, produced, or manufactured in the U.S. This percentage is a minimum threshold to qualify for the bonus credits

Project developers need to ensure compliance with the domestic content requirements to qualify for the bonus credits. This involves detailed documentation and verification that the materials and products used in the construction meet the specified criteria. The U.S. Treasury Department, along with the Department of Energy, provides guidance and oversight to ensure that projects claiming the bonus credits adhere to the requirements.

Exact system and resources requirements >>

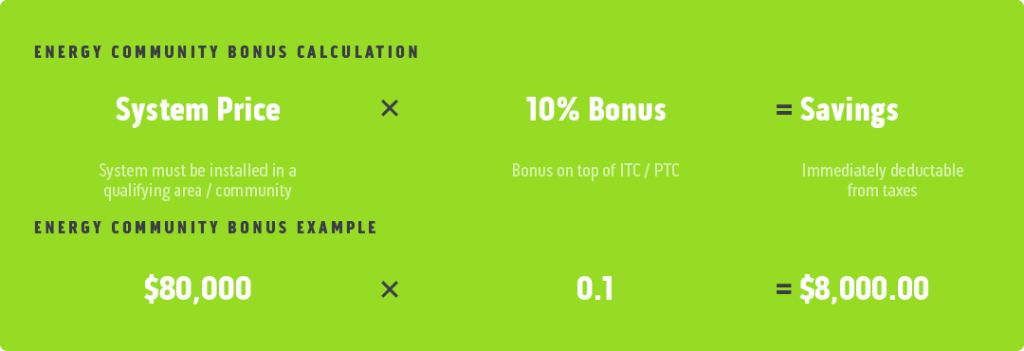

Energy Community Bonus

The Energy Community Bonus is designed to stimulate economic recovery in areas that have historically relied on fossil fuel industries such as coal, oil, and natural gas. This includes regions impacted by the closure of coal mines or coal-fired power plants. A major outline of the program states:

- Eligibility: Projects that are located in designated energy communities qualify for this bonus. These communities are typically characterized by high unemployment rates or significant job losses in the energy sector.

- Benefit: Qualifying projects receive an additional 10% bonus on top of the standard tax credits available under the Inflation Reduction Act. This applies to both the Investment Tax Credit (ITC) and the Production Tax Credit (PTC).

- Objective: By offering this bonus, the government aims to redirect investments towards these communities, helping to diversify their economies and provide new employment opportunities in the growing renewable energy sector.

The U.S. Department of Energy hosts a mapping tool that identifies energy communities. These are areas affected by the decline of coal and other fossil fuel industries. The map includes census tracts with historical ties to the fossil fuel industry and those that have experienced significant job losses in these sectors. This tool is crucial for determining eligibility for the Energy Community Tax Credit Bonus, which provides additional incentives for renewable energy projects in these areas. You can explore this through the Energy Communities website, which includes tools and resources to identify qualifying communities.

Interactive Map with qualifying areas / communities >>

Low-Income Community Bonus

This bonus aims to increase access to renewable energy technologies in low-income communities, which often face higher energy costs relative to their incomes and are more vulnerable to environmental hazards. What you need to know:

- Eligibility: Projects located in low-income communities or serving these areas are eligible. This includes solar and wind installations that directly benefit residents, such as community solar projects where multiple households can benefit from a single installation.

- Benefit: The Low-Income Community Bonus can add a significant percentage to the base ITC or PTC — up to 20% additional credit, depending on the specific details of the project and its impact on the community.

- Objective: The focus here is on reducing energy costs for low-income households, promoting energy equity, and ensuring that the benefits of renewable energy expansion reach all segments of society.

The Low-Income Communities Bonus Credit Program is managed by the Department of Energy in partnership with the Treasury and the IRS. This program offers increased investment tax credits for renewable energy projects in low-income areas. The Department of Energy provides resources and application guidelines for this program on their website. Additionally, there is a specific mapping tool available that helps identify eligible low-income communities where projects can qualify for increased tax credits

Interactive Map with qualifying areas / communities >>

Let’s Apply That to a Real System

Incentive

Price Deduction Percentage

Price Deduction

Absolute

Investment Tax Credit (ITC)

30%

$24,000

MACRS Depreciation Benefit (Over 5 Years) *

10.35%

$8,280

Energy Community Bonus

10%

$8,000

+ Additional, state-specific incentives of up to 25%

Total Tax Deduction

50.35%

$40,280

*at a federal tax rate of 23%

HelioWing 7 – 9.84 kWp System

Premium, all-integrated Solar Carport

$80,000

MSRP

Incentive

Price Deduction Percentage

Price Deduction

Absolute

Investment Tax Credit (ITC)

30%

$18,000

MACRS Depreciation Benefit (Over 5 Years) *

9%

$5,400

+ Additional, state-specific incentives of up to 25%

Total Tax Deduction

39%

$23,400

*at a federal tax rate of 20%

HelioWing 5 – 7.38 kWp System

Premium, all-integrated Solar Carport

$60,000

MSRP

Conclusion

In conclusion, navigating the landscape of federal incentives for solar energy in 2024 can provide substantial financial benefits to businesses and individuals looking to invest in renewable energy. The variety of incentives available, including the Investment Tax Credit (ITC), Production Tax Credit (PTC), and MACRS depreciation, are designed to reduce the cost barriers associated with solar installations and promote a shift towards sustainable energy solutions. Additionally, specialized incentives like Direct Pay and the Domestic Content Bonus further enhance the attractiveness of these investments by supporting domestic manufacturing and providing immediate financial returns to eligible entities.

Understanding and utilizing these incentives not only aids in achieving financial savings but also contributes to the broader goals of energy independence, environmental sustainability, and economic growth through job creation in the renewable sector. As the solar industry continues to evolve, these incentives play a critical role in shaping a greener future, making now an opportune time for potential investors to consider how solar energy can fit into their long-term strategic plans.

FAQ’s

What is the maximum amount of benefits from federal tax incentives?

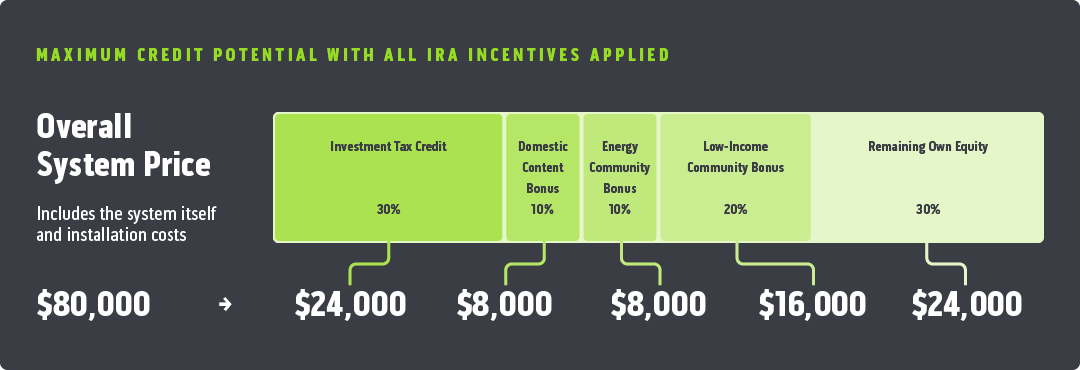

Although it is very unlikely for a project to qualify for all available federal incentives and bonuses for solar energy systems (ITC, Domestic Content Bonus, Energy Community Bonus and Low-Income Community Bonus), the highest possible tax credit would add up to 70% of a systems price. However, adding state-specific incentives to the available federal incentives might bring even greater financial benefits. You can find a list of state–specific incentives by U.S. state here.

Can the Production Tax Credit (PTC) be combined with the ITC for solar projects?

No, the PTC cannot be stacked with the ITC. You must choose one or the other. The PTC offers a per kilowatt-hour credit for the electricity generated by your solar system for the first ten years of operation, which is beneficial for projects with high energy output and efficient operational conditions.

How does MACRS work for solar systems, and what is the bonus depreciation in 2024?

The Modified Accelerated Cost Recovery System (MACRS) allows for the accelerated depreciation of solar PV systems over a five-year period. In 2024, solar systems can qualify for a 60% bonus depreciation, which is a significant tax advantage as it allows for a larger portion of the asset’s cost to be depreciated in the first year of service.

What is Direct Pay and who is eligible for it under the solar tax incentives?

Direct Pay is a provision that allows tax-exempt entities, such as non-profits, state and local governments, and tribal governments, to receive the value of certain tax credits as direct payments instead of tax credits. This is particularly advantageous for organizations that do not have significant tax liabilities and enables them to benefit directly and immediately from solar incentives.

What are the benefits of the Domestic Content Bonus for solar projects?

The Domestic Content Bonus provides additional incentives for using American-made products in solar projects. Eligible projects can receive an extra 10-percentage-point increase on the ITC or additional credits under the PTC. This not only supports the U.S. manufacturing sector but also adds financial benefits to the project’s bottom line.

More relevant posts for you